New EU and international data show long-term production decline, persistent price pressure, and an incomplete recovery in consumption.

Greece’s olive oil crisis is no longer a short-term shock followed by recovery. New production data and long-range forecasts released in late 2025 and January 2026 indicate the country is entering a prolonged period of structural decline driven by climate pressure and systemic production constraints.

While output rebounded temporarily in 2024–25, forward-looking assessments now show declining volumes, incomplete demand recovery, and a new price baseline well above pre-crisis levels.

Production collapse and a fragile rebound

The crisis began with a sharp climate-driven production collapse across the Mediterranean.

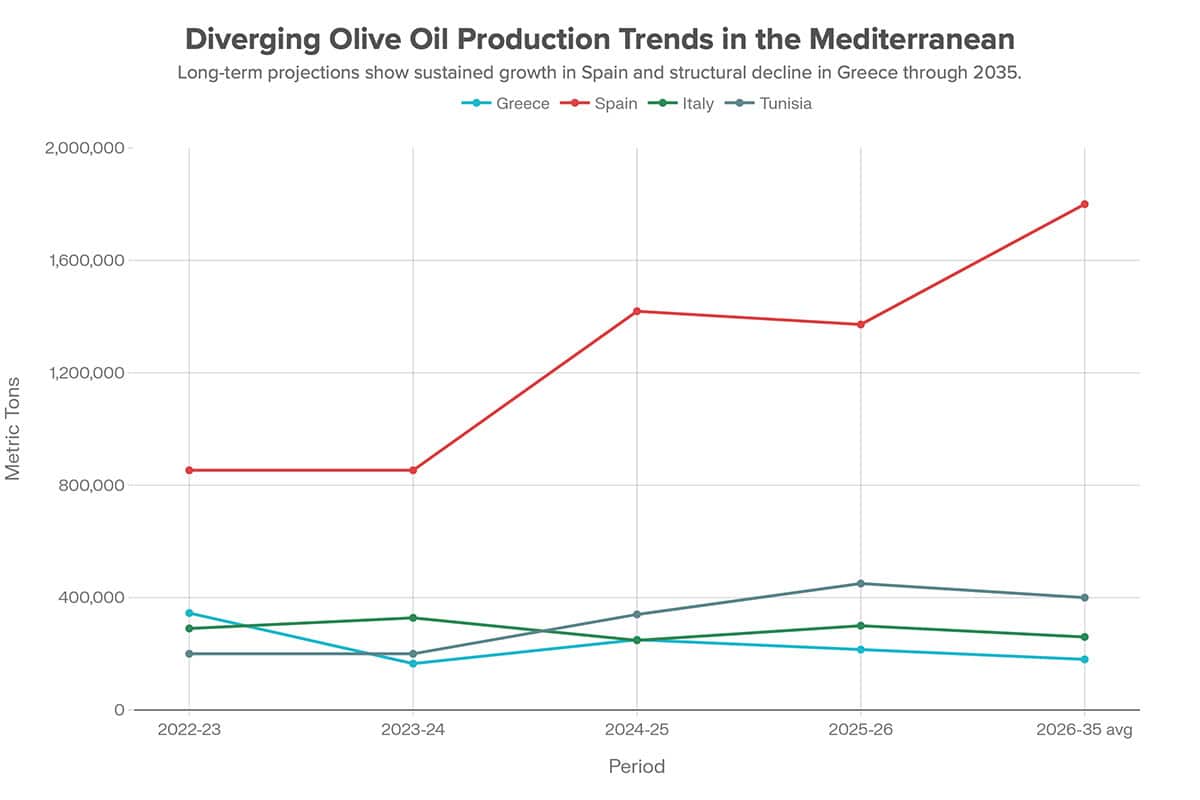

According to data from the International Olive Council and EU agricultural reporting, Greek olive oil production fell from approximately 345,000 tons in the 2022–23 season to an estimated 155,000–175,000 tons in 2023–24, one of the weakest harvests in decades.

The following season brought partial relief. Output in 2024–25 reached roughly 250,000 tons, confirmed by national and EU data. However, this rebound now appears temporary rather than indicative of a stable recovery path.

New reporting from January 2026 indicates that the 2025–26 harvest is already unfolding under renewed biological stress. Late-autumn rains and elevated humidity have intensified olive fruit fly pressure and fungal infections, particularly gloeosporium, resulting in fruit rot, lower yields, and quality losses across several regions. Producers in parts of the Peloponnese and western mainland Greece report yield declines of 30–35 percent compared to the previous season, with mills encountering higher acidity and increased rejection rates for extra-virgin classification, according to reporting by Olive Oil Times.

Production forecasts for 2025–26, compiled between October and November 2025, suggest renewed decline:

- Optimistic estimates: 240,000–250,000 tons

- Most realistic range: 210,000–230,000 tons

- Expert assessments: closer to 200,000 tons

More significantly, the EU Agricultural Outlook published in January 2026 projects that Greek olive oil production will average below 180,000 tons annually through 2035, constrained by “climate pressures and structural limitations.” This reframes the crisis as a long-term contraction rather than a volatility cycle.

Regional divergence inside Greece

National averages obscure sharp regional differences.

Preliminary 2025–26 estimates indicate:

- Peloponnese: approximately 90,000 tons

- Crete: approximately 50,000 tons, with continued vulnerability to drought and olive fruit fly infestation

- Islands and mainland regions: a combined 60,000–90,000 tons

Crete, historically one of Greece’s most important olive-producing regions, faces persistent pest pressure and water stress, raising concerns about sustained output decline even in average rainfall years.

Climate, pests, and labor constraints

Climate instability remains the primary driver.

Multi-year drought, erratic rainfall, and prolonged heatwaves continue to disrupt flowering cycles and fruit development. These conditions also favor the olive fruit fly (dakos), increasing infestation rates and lowering oil quality through elevated acidity.

During the 2025–26 harvest, these dynamics materialized directly, with late-season humidity accelerating pest and fungal spread and contributing to measurable yield and quality losses reported by producers.

Economic constraints compound biological stress. Harvest wages rose gradually over several seasons, increasing from roughly €40 per day to €70–80 by 2023–24. At the same time, yields in affected areas fell by as much as 60–70 percent.

As costs rose and yields fell, harvesting became uneconomical for many producers. In affected areas, leaving fruit unharvested became a rational response to negative margins rather than an isolated exception.

Prices: stabilized, not normalized

Wholesale prices peaked in mid-2024 and have since fallen sharply. By late 2025, prices were down approximately 62.8 percent from their July 2024 highs. However, stabilization does not equal normalization.

Retail prices in 2024–25 averaged €7–8 per liter, compared to €4–5 per liter before the crisis in 2022. Despite falling wholesale prices, retail pricing adjusted slowly due to inventory lag, contract structures, and higher baseline production costs.

The result is a new equilibrium: prices are more stable but remain 50–100 percent above pre-crisis levels, reinforcing the view that the crisis reset the market rather than resolving it.

Consumption decline proves persistent

Consumption fell sharply during the price spike. Nationally verified data indicates a decline of approximately 26–27 percent during the peak of the crisis. Higher declines approaching 40 percent appear in lower-income and high-price regions but are not nationally representative.

As of January 2026, recovery remains limited:

- Only about 25 percent of lost consumption has returned

- Roughly 75 percent of the reduction persists

Household behavior has adjusted structurally. Consumers increasingly favor bulk metal cans, direct purchases from producers, private-label oils, and reduced daily use. These shifts suggest adaptation rather than temporary restraint.

Labeling, fraud, and trust concerns intensify

Higher prices have intensified scrutiny of labeling and origin. According to EU Rapid Alert System notifications and Italian enforcement disclosures from 2025, recent investigations have highlighted persistent weaknesses in origin labeling and traceability across the olive oil trade.

That enforcement data strengthens long-standing concerns:

- Italian authorities detected 72,000 kg of unregistered olive oil

- 3.6 tons of Greek-origin oil were seized in Bari lacking mandatory origin indication

- 39 of 182 EU fraud notifications involved Greek olive oil products

While not all cases involve consumer deception, the data underscores persistent opacity in origin, bottling, and value transfer across borders. As prices rise, trust becomes a central market variable.

A long-term decline, not a temporary shock

The revised data alters the narrative fundamentally.

The 2024–25 rebound provided temporary relief, but current forecasts point to declining production, persistent consumption loss, and elevated price baselines. According to EU projections, Greece is entering a prolonged period of reduced olive oil output, while competitors such as Spain and Tunisia are expected to maintain or strengthen their positions. Italy, meanwhile, faces its own projected annual decline of roughly 3 percent.

For Greece, the olive oil crisis is no longer about recovery. It is about adjusting to a smaller, more volatile, and more constrained future, shaped by climate realities and embedded limits unlikely to reverse.